Variance and Standard Deviation: The Mathematics of Bankroll Volatility on 7XL

In the Tier-1 quantitative architecture of the 7XL VIP poker network, winning is never determined by a single session. It is an algorithmic inevitability stretched over infinite computational cycles. However, the bridge between short-term execution and long-term Expected Value (EV) is inherently hostile and highly volatile. Level-0 players are financially annihilated by downswings because they treat the ecosystem like a casino, lacking the structural infrastructure to absorb the shockwaves of pure probability. True Alpha-Architects understand that volatility is merely defined by Variance and Standard Deviation. This manifesto dissects the uncompromising risk management protocols required to bulletproof your liquidity pool against catastrophic mathematical tail events.

Phase 1: The “Whys” – Decoding the Statistical Noise and 3-Sigma Events

Why do elite, perfectly unexploitable GTO (Game Theory Optimal) operators experience massive, account-draining financial drawdowns? The answer lies in the uncompromising physics of the Central Limit Theorem and statistical dispersion. Expected Value (EV) dictates exactly what you should mathematically win over an infinite timeline, but Variance is the brutal dispersion of actual, kinetic results around that expected mean in the short term. In a high-stakes, hyper-liquid ecosystem like 7XL, your standard deviation metric is the ultimate defining factor of your structural pain tolerance.

Downswings are not algorithmic curses, rigged generators, or “bad luck.” They are a mathematical guarantee built into the very fabric of probability. When you deploy multi-route execution strategies—such as aggressively deep-stacked VIP cash games or ultra-high-variance Spin & Gold tournaments—your true win rate (measured in bb/100) acts as your system’s propulsion engine, but your standard deviation acts as the atmospheric turbulence. If your liquidity pool (bankroll) is not structurally engineered from the ground up to withstand a 3-standard-deviation event (a 99.7% statistical extreme parameter), you are operating a highly fragile, doomed system. Understanding the exact “Why” behind mathematical variance instantly purges emotional bias (tilt) from your mental DOM. You stop trying to fight the cards and start accepting standard statistical noise generated by the mathematical fabric of the Tier-1 matrix. You do not survive variance; you out-compute it.

Phase 2: The “How-Tos” – Engineering Quantitative Resilience

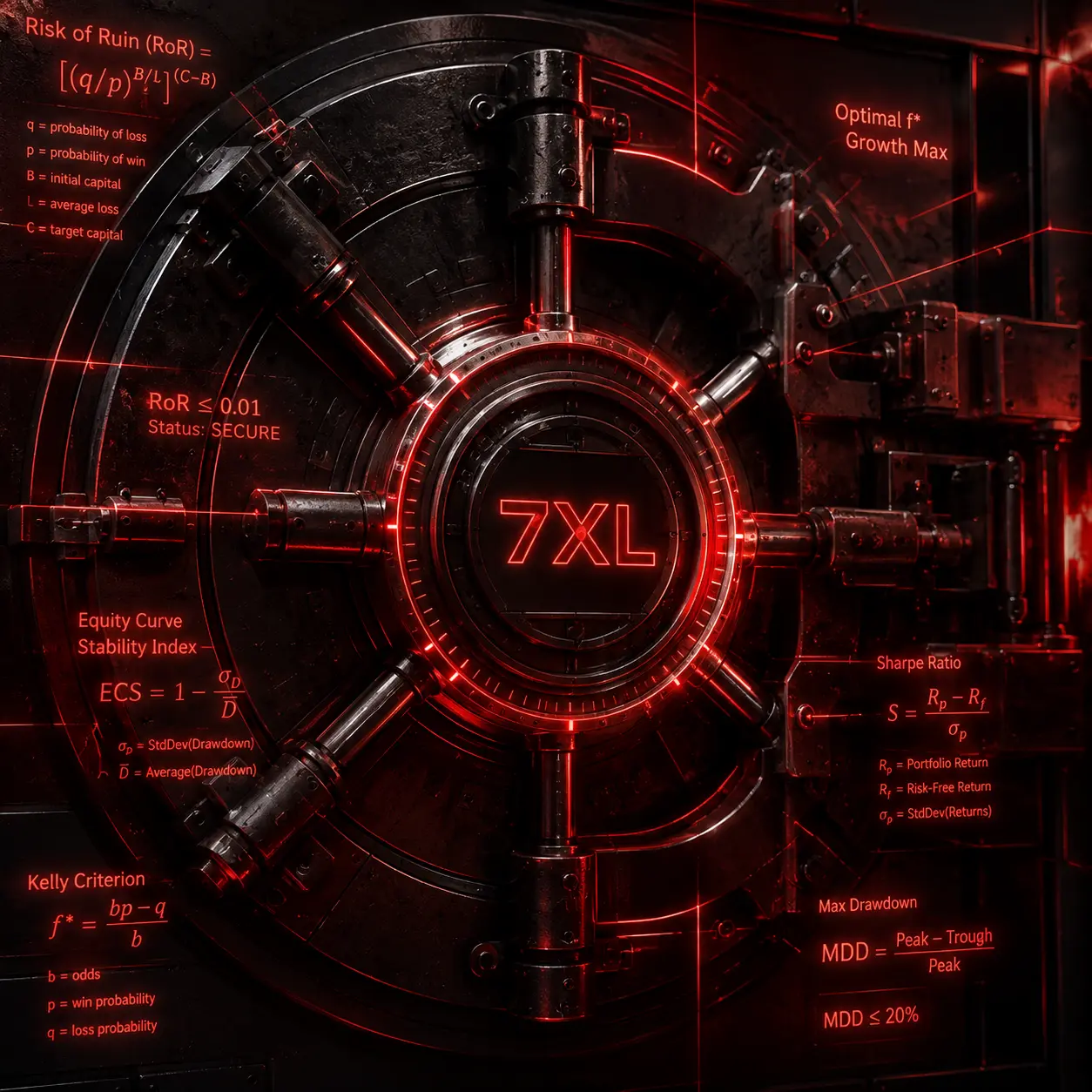

How do you translate abstract standard deviation data into an actionable, kinetically bulletproof bankroll strategy? You must immediately abandon Level-0 logic and deploy the precise Risk of Ruin (RoR) algorithmic formula. The outdated, generic rule of “always have 100 buy-ins” is a fragile myth designed for amateurs. Your required liquidity threshold must dynamically scale based on your exact, real-time win rate and standard deviation metrics, which must be extracted directly from your 7XL Smart HUD after a statistically significant sample size (an absolute minimum of 100,000 algorithmic cycles).

First, isolate your true standard deviation. If you are deploying an aggressive, high-VPIP (Voluntarily Put In Pot) exploitation strategy, your variance multiplier will spike violently, necessitating an exponentially larger capital reserve to maintain a Risk of Ruin below 1%. Second, implement a strict Fractional Kelly Criterion sizing model. Instead of risking the mathematically optimal percentage of your bankroll on a single tournament grid or cash table—which exposes you to catastrophic sequence risk—you must risk only a precise fraction (e.g., 25% or 30% of the Kelly suggested volume). This protocol drastically reduces the kinetic impact of standard deviation spikes while still maximizing compounding capital growth. You must re-wire your brain to treat your bankroll not as fiat money, but as pure ammunition for a continuous, high-frequency mathematical siege. When variance inevitably pushes your data into a severe drawdown, your fractional sizing protocol must automatically, without emotion, trigger a downsizing event. Scaling down limits when your liquidity drops ensures absolute systemic survival, completely immunizing you against the ultimate failure state: bankruptcy.

Phase 3: Pro Tips – Advanced Institutional Risk Protocols

Integrate these Tier-1 cryptographic rules into your execution logic. The subtext is critical:

- 1. The Kelly Override: The Fractional Kelly protocol completely fails if your standard deviation exceeds your structural baseline—are you tracking your spikes?

- 2. Data Corruption: Never calibrate your Risk of Ruin metric using a sample size smaller than 250,000 hands; smaller datasets are algorithmic hallucinations.

- 3. The Sigma Threshold: A 4-standard-deviation downswing requires an immediate cessation of your current tier limits—do you know your exact trigger threshold?

- 4. Liquidity Illusion: If your win rate is artificially inflated by local, soft liquidity, your variance models are already fatally compromised.

- 5. Static Vulnerability: Institutional capital never relies on static bankroll parameters; dynamic, intra-session downsizing is your only shield against black swan events.

- 6. The Fatal Loop: The exact microsecond you attempt to manually “win back” variance, your architectural integrity drops to absolute zero.

Execute Your Mathematical Edge

Theory without execution is a computational waste. Deploy your structural bankroll strategy in the world’s most aggressive liquidity pool. Join the 7XL Tier-1 network.

REGIONAL GATEWAYS: TIER-1 ACCESS NODES

- ▶ UAE High-Stakes Gateway

- ▶ Brazil Institutional Liquidity

- ▶ Pakistan VIP Poker Infrastructure

- ▶ Turkey Crypto Poker Node

- ▶ Israel Tier-1 Access Protocol

- ▶ Global Ecosystem Gateway

TACTICAL INTEL & ADJACENT NODES

Return to Core Command: 7XL Poker Architecture & Core Systems

- ▶ Active Payload: Systemic Mathematics of MTT Variance

- ▶ Active Payload: Quantitative Table Selection & EV Architecture

- ▶ Active Payload: The Architecture of Decision (EV vs. Emotional Bloat)

- ▶ Active Payload: ICM Poker Strategy on 7XL Final Tables

- ▶ Next Node: Exploitative Heuristics & Deep-Data Network Analysis